“Well, frankly, you’re the worst, and it’s not close.”

A conversation with a client turned into a direct research and design project. I asked how Espírito Santo Bank (ESB) stacks up against its competitors, and the answer was eye opening. Even more eye opening, ESB had not previously conducted client feedback studies of any kind. It was flying in the dark…

intro

Imagine applying for a credit card and the decision takes nearly a year to arrive.

ESB’s trade finance team would provide loans to small/medium sized companies in Latin America. It took 10 months, on average, from application to first disbursement! So, what can a bank considered a “relationship bank” do to improve? It can start by actively asking clients to honestly give feedback…

Designed an online form reducing time needed to structure a loan and disburse funds by ~30% . I used surveys, client interviews and a pilot to gather data. Key deliverables were persona development, user journey map, user flows, wireframes, prototypes and a working online form.

the tldr:

the problem

“You all take too long. By the time the loan is structured, we’ve sent massive amounts of emails, and you then start asking for more documents!”

-Chief Financial Officer, Undisclosed large client

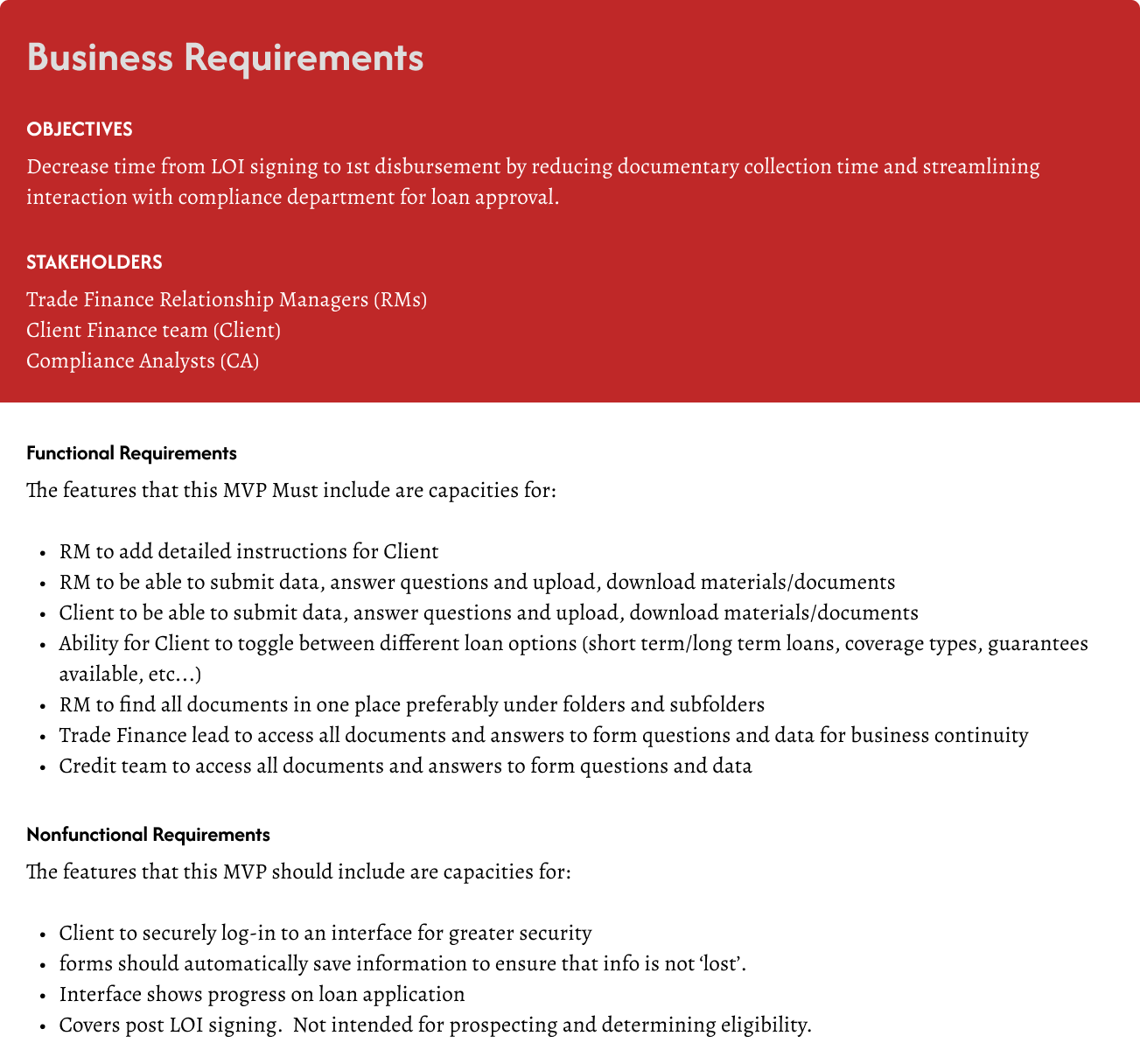

THE GOAL

Understanding Why a Client was so disgruntled

The CFO of an existing client said:

“Well, frankly, you’re the worst, and it’s not close.”

”Why?” I asked.

He answered: “[your bank] take[s] too long. By the time the loan is structured, we’ve sent massive amounts of emails, and you then start asking for more documents!”

My goal was clear: Reduce the time from Letter of Intent (LOI) to first disbursement.

THE hurdle

Culture…

ESB prided itself on being “a relation bank”. I was brought on to help the team integrate a lead generation service onto our CRM’s database. Other banks had done this years ago. It wasn’t the most techie bank on Brickell, Miami’s finance district.

There was pushback starting this project but, I ended up with evidence that the client--our persona--was not the one who signed the contract. The business owner wasn’t “the user”. Once the sales pitch was over, and the LOI signed, we interfaced exclusively with the the finance department. This was our “user”. We needed to satisfy THEM.

the research

"I sent it already in an email last Thursday. It was one of 7 emails I sent you that day."

-Director of Finance of a Mexican PYME

Stepping back

Are These Just “Sour Grapes”?

I needed to dispel my biggest fear with qualitative research: Is feedback just an anecdote from a disgruntled client (we’d cut his line by 30%) or all throughout? I wanted a sense of security that only quantitative methods grant—a brief survey. I asked the Relationship Managers (RMs) to participate in a customer satisfaction survey. I needed to get their buy in so their input was sought early to develop the survey. We came across 7 dimensions of concern. These were:

The time to structure (my contribution)

Time to disburse (my contribution)

The loan amount

The term of the loan

Guarantees required

Documentary burden

Covenants imposed

I then built a 15 question survey with two questions per dimension above and an open ended question on our overall performance to capture aspects that we missed. Each RM distributed the survey via email and personally reached out to both the CEOs and the CFOs to fill it out. It was a more personal touch than generically blasting their inboxes and would increase the response rate, I thought. The results were as follows:

-

responded “Worst than other banks” regarding Time to Structure a loan! Second highest with that response was Time to Disburse--both document heavy processes. Yet, we were “about the same as other banks” (64% of responses), for Documentary Burden. So, ESB wasn’t asking for too much…it wasn’t collecting properly.

-

In the survey’s open response, a frequent complaints was the process whereby we asked for proof of ownership. KYC and AML regulation require this. Commercial loans require that articles of incorporation be submitted. This can be hard, especially if the owner is a High Net Worth individual who seeks anonymity.

We would need to do something so that the structure would be laid bare at the point of application. This was a pain point for clients and internal employees alike!

-

So, if the process is burdensome, imagine having to do this every year! Revolving lines of credit were typically structured for one year terms.

In the open ended question, many complained that we asked things “as if we had just met.” we needed to work with credit and loan insurers to ask only for the minimum amount of documentation to support renewing the credit line. -

Of the roughly 150 surveys sent, only 9 CEOs responded. Five of these responded with a variant of: “talk to my director of finance.” It was clear that the CEO just wanted to get shipments paid with the line of credit. They didn’t want to deal with the bank. This makes all the sense in the world, but it would take some convincing to change this mindset within the team.

What i learned

Given the results of the survey, it was clear to me that:

CFOs/finance directors are our persona, NOT CEOs

It’s not the amount of docs, but how we gather them.

There is a trust issue. I need to know why.

Email for document gathering, not a good idea. We need a central repository.

I wanted to interview 5 of the most disgruntled respondents. Three of which were not clients I managed, so I’d have to be sensitive to how I conduct these. I needed to know:What do other banks do right, what do we get wrong.

Oh, and why the distrust??

I also needed to sit down with other RMs to get their version of why it takes us so long to structure credit. I knew from my experience that:Receiving necessary documents was time consuming, weeks could be wasted here.

Credit department risk assessment was lengthy and out of our control.

Loan insurance agency approval of coverage took many weeks or months.

Compliance, well, where do I begin...? It was often a black hole where loans went to die.

Exporters providing necessary documents for letters of credit or disbursement was also a catching point.

So, I would need to sit down with stakeholders in credit, compliance and insurance underwriters. This was going to take a while and was not going to be a linear process. I knew this going in. There are too many stakeholders in this chain of events for this to be simple. As far as budget, it would be inviting others to a lunch, or meeting up at a restaurant when a client was visiting Miami, or I was visiting them. The bank was not allocating a dime to this!!

After a span of 7 months, these were the outstanding quotes to share:

“We were 20 emails deep when I just gave up and gave him access to my shared drive and said, put it all in there.”

This (SERIOUS) security faux pas represents a user, in this case another RM, finding a way to share documents. They “satisficed” by sharing their shared drive with titles and all to give their client’s finance team somewhere to put the docs!

“I hadn’t seen the docs until I came back from PTO. So, credit received the package about 10 days late. ”

By having only email as a way to transfer docs, if the email’s account holder, for whatever reason, didn’t pass on the docs, the whole process would be stalled.

“Man, these articles of incorporation are impossible to follow. There are shell companies to shell companies...”

With all the shell companies, it could take a week to unravel legal structures. Since we were dealing with many countries in the LATAM region, laws varied. We needed a way for the company help connect the dots.

“[another banks has] an online portal where you go in and just answer questions there and upload documents. It’s easy.”

This was a client talking about how one of our competitors solved these issues. They were a peer bank with about as much resources, but their management was more open to “tech solutions”.

KNOWING IS (part) OF THE BATTLE

BUT KNOWING YOUR PERSONA IS WINS EVERYTIME!

It was now time to get buy in. I presented the new user persona, and a user journey map to describe the client’s pain points, enhance by internal staff quotes to show context and motives for the poor service.

Click to view image detailKNOWING IS (part) OF THE BATTLE

BUT KNOWING YOUR PERSONA IS WINS EVERYTIME!

Click to view image detailWe now had a central document to rally around and discuss more concretely where work was needed. It was now clear that the most important thing to improve was the document collection process, and improving our ways-of-working with compliance. I also learned other banks were completing the process in 6.5 months! We now have a goal.

With Manuel, our persona, we needed to be direct, and provide clear, up-front instructions when requesting documentation. Remember, he wants to spend more time with his grandchildren, so no surprises. Any bad news...up front, no matter how large the documentary burden! If you think that’s trivial, consider that some RMs preferred to ask for documents “in doses”, so as to not create alarm in the client’s finance department. This persona was going to challenge that!!

the solution

“We like interacting with out clients. They also like interacting with us. Our clients are very rate sensitive, but it’s the relationship that keeps them here.”

-Head of Trade Finance

START FROM SCRATCH...AND ON YOUR OWN.

Although the department lead had the opinion above, he now saw that there may be room for improvement. He saw the urgency but, he was very clear, there’s no budget for creating an online tool. I anticipated this and told him that I could build an online application form as a proof on concept...an MVP. Honestly, the ideation of the solution wasn’t much of a process. The interview phase revealed that the best experiences came from online application forms...

But first, let’s gather the requirements for this online form so that it can be pretty, pretty, pretty good!

before wireframes, know the flow!

Plan It First!

Before any wireframes, I need to understand the logic for this online application to work. Nothing better to understand step-by-step procedures than drawing it out in a work flow / diagram. See mine here:

Click on image for detailOnce I had the flow in place, it was pretty simple to think about how to design the online application form. I made some wireframes versions and got feedback from other RMs. The following version is the one that most resonated because of the progress bar, the page by page structure so as to not overwhelm the client and the clean, uncluttered look.

this is crucial!

There are interfaces you MUST get right…

One page that proved to be particularly important was the ownership structure page. It’s wireframe went through many iterations of internal testing with multiple versions. RMs and Compliance staff were closely involved in its design.

Click on image for detailNo other RM really wanted to test the interface with their clients, so I would choose two of my own clients--ones that I was particularly close with--and get their reactions. After presenting these wireframes to them, and going over the flow, they had a few suggestions. Namely that they would feel a bit strange asking their suppliers to also log in and load their documents. I pivoted and had our own documentary specialist use the form for submitting the documents once she got them. She was also complaining that she got her docs piece-meal and would like a way to organize these better. This was something that I would have to think through a bit better but, this was not a showstopper.

USING AN OFF-THE-SHELF SOLUTION

Since no budget would be dedicated to this project, I resolved to use an off the shelf tool. Outlook had a form builder but, frankly, it was a bit complicated to use. One that was available at the time and relatively easy to use was Jotform. It had some limitations, but I would be able to use a lot of the features that is supported to my advantage, although my wireframes would have to be modified slightly. We forge on! WE ONLY NEED A PROOF OF CONCEPT.

HOW I WANTED TO DESIGN IT

fire up figma!

Show the Rough Draft of Your Ideas

I knew that I would build my MVP in an off-the-shelf tool. However, I was excited to build a web-based application form, so I mocked it up. These mock-up pages also formed a basis in case the bank wanted to throw some budget behind them. Note: It’s in Spanish since over 90% of our clients were from Spanish speaking countries in LATAM region, and in Mexican legal terms, since Mexico was about 60% of our clients and 77% of our outstanding loans.:

HOW I WANTED TO DESIGN IT

HOW I WANTED TO DESIGN IT

DESIGNING THE MVP

With the mockups in hand, it was pretty easy to build the online application form so, no waste in making the mockups! Jotform was really easy and had the page setup that I wanted for a less overwhelming, ‘step-by-step’ feeling for our end user. It even allowed me to incorporate a progress bar!

SO...NO USABILITY TESTING?

Actually, there was none. I decided to pilot the online application with two upcoming renewals and three new applicants. All of the testing was done with internal stakeholders to reveal “silly” mistakes (and there were a few...). Also, I learned that the files downloaded were not neatly placed into folders, but they were at least present in the dashboard in an orderly fashion. That alone was a big upgrade over pouring through emails to find attachments and answers to questions. I’ll give results in the next section: “The Takeaway”.

the takeaway

Word arrived that no new credit packages would be processed as the bank was being sold. Only packages already approved by credit would be allowed to continue. Thankfully, my “Pilots” had already cleared the credit department! In part because:

-

The roughly 16 weeks that the credit packages took to get approved, now took on average 13 weeks under the new process design. The last package cleared that announcement by just over one week!

-

I eliminated email that I identified as “informational”--defined as emails where business specific information was requested. IT WAS ALL IN ONE PLACE AND STRUCTURED! No more need to read through paragraphs to arrive at a nugget of data.

-

A client’s employee that was often tasked with gathering docs was “extático” when he learned that he would not have to .zip and reformat documents so that they could properly attach to email. He could load the exact document at the exact section where it was relevant and not have a data ceiling on attachments.

-

The approval rate of the 5 pilot clients. Ultimately, the 5th client that was pending, had to re-apply with another bank since ESB Florida was ultimately shuttered. But, the traditional approval rate had always hovered around the 60 - 70% mark.*

*Apporval rate was not a metric that I had sought to affect and I really cannot draw strong conclusions here with such a small sample size.

The strongest case for how effective the new process design was came from there being no clear benefit to new vs. renewing clients. They BOTH showed strong improvements in time reductions.I always say I’m a glass half full kinda guy, but I can’t help but be cautious or at least doubt my results. Overall, the time reductions from LOI to disbursement was reduced by roughly 30%. A lot of that time reduction happened in the documentary collection stages and the compliance stage--those lunches with compliance worked out! I was able to gauge what compliance needed and when they needed it better and thus, design a better form.

But the biggest takeaway?? Since I was the designer, I was more invested in the design and wanted to see it succeed. Therefore, I would not be completely satisfied with these results until other RMs also implemented this new process design. I can imagine push-back to change and simply the learning curve of using another platform, no matter how simple it was.

LOW BUDGET TO NO BUDGET. NO PROBLEM!

I was never put off by the fact that no budget would be set aside for this project. ON THE CONTRARY! I was glad that my enthusiasm was curbed and that I ran a pilot with a no-code online form. This led to ‘quick-data’ to hammer out any remaining kinks. The pilot’s ‘renewal’ clients commented on the new process. They approved, although, maybe because they were accustomed to interacting over the phone, they still reached out for questions that were clearly (to me at least) covered in the application process. This would form the basis for my subsequent iterations, had the unthinkable not happened... BES Lisbon ran afoul of regulators and was forced to liquidate subsidiaries, including ESB Florida.

But did you notice? There were no research costs. I didn’t spend a cent on surveys, interviews or usability tests--well maybe a couple of lunches with my colleagues in compliance. The linear product development model is taken as sacred by too many designers. I think there should be an ‘as necessary’ approach to research and design. Understand the risks of getting it wrong, the cost of getting it right, and find a happy medium. I determined that the cost of getting my MVP wrong would just cost me more late days in the office processing the application. I could live with that if I could find a way to cut time from LOI to disbursement by at least 10%, since 10% was our annual loan disbursement growth goal. This would be about a month. So, what did I get for my efforts?

WELL, THAT WAS UNEXPECTED...

other case studies

No time to waste, yet everything to gain...

When tasks in an educator’s day can take them away from their ultimate joy, we need to take stock. See the insights and designs that let educators interface more with their kiddos!

A story of a startup not letting vacation planning to chance.

This story began with a founder wanting to find out what to do when Friday rolled around. Research revealed that, if he faced a challenge, it paled in comparison to those traveling abroad.